If you are having trouble understanding the insurance claim document you have on file for the damage that has occurred to your property, you’re not alone! Insurance claims are confusing. There are a bunch of terms and many of them don’t make any sense, there are a bunch of sections that don’t seem to relate to anything meaningful, and there is an endless array of dollar amounts and they oftentimes don’t seem to add up. But don’t worry, we’re here to help!

This insurance claims document is actually made up of two parts: the estimate pages and the insurance policy. The insurance policy tells you what your insurance company will pay for and the estimate pages tell you how much it will cost to repair or replace your damaged property.

The insurance policy can be very difficult to understand. If you have any questions about what your insurance policy covers, you should contact your insurance agent or company representative. They will be able to explain the terms of your policy and what it means for you.

The estimate pages, on the other hand, are much easier to understand. These pages itemize the damage that has been done to your property and gives you an estimated cost of repairs.

We began this series of articles recently to explain insurance claim documents and you can read the previous article here.

If you’re mystified or intimidated by your claim document, hopefully we can help clear up the confusion in this article.

FILE #: 144375280

Insurance Documents are Confusing

When you obtain an insurance claim its best to review it and make sure your damage report is covered, your proof is applicable, you gave your insurance provider the documents required for the claim, and your insurer is aware of the circumstances that led to your claim.

Let’s walk through a claim form so that when you get a document from your insurance provider it will all make sense to you.

Many insurers will use Xactimate to write their estimates. This blog will explain the details of a claim created by that Xactimate. The estimate of the overall cost of the property damage section of the claim document was originally intended to be just that – an estimate. It was intended by the company which designed the estimating software, Xactimate, to be a “budgetary document” to provide a foundation, or a stepping-stone to start the conversation about the scope of work and potential costs for the property restoration. It was supposed to be a starting point, not an ending point.

Now, however, the insurance companies tend to want to use this document as their “stone tablets” with the 10 Commandments written on them and many times will try to convince homeowners and contractors that they can’t make any changes to these documents. This actually isn’t the case. If your professional contractor is involved, he or she will know what information or documentation an insurance company needs to correctly scope your loss, easing the process of filing a claim in the future.

FILE #: 423791317

Summary Page

The first page will show the insurance company information, the claim number, and show homeowner information and the adjuster information and all the contact info. The other major thing Xactimate does is it shows a price list. This is a particular code that shows the version Xactimate used, plus the location and date. This is important because it shows the timeline between the damage done and when the claim was filed. By the time the work begins, it could be a year later, they will need the prices at the time of the job and not when the damage occurred.

Some of the other stuff you’re going to see on here are numbers which include the cost of your claim, i.e. the total of the line items that are adding in tax, the total claim amount, and then they depreciate it.

Depreciation is essentially the amount of money that insurance companies are keeping back out of the claim that they will pay when the work is done. The next number is the actual cash value— that’s the replacement cost minus the depreciation. Following that is the deductible, and then the net claim. Next, total recoverable deprecation; that tells you how much money you will get back when the work is done. In contrast, if it says non recoverable depreciation, you have an actual cash value policy, therefore you won’t get any money back for the work done and will only receive the claim amount i.e. net claim. The last line says the net claim if deprecation is recovered, excluding the deductible, which is the total claim amount you will get under an actual cash value policy.

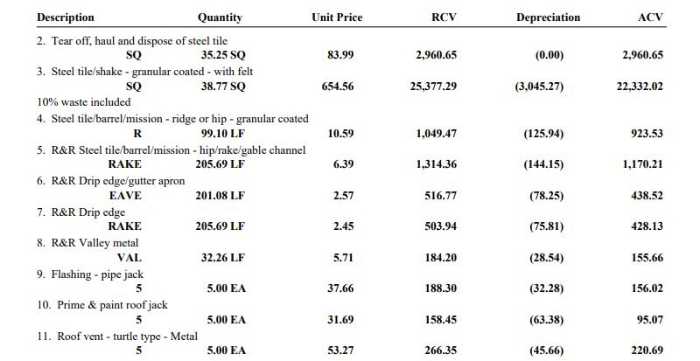

The Actual Estimate Break-down

Next you will see the line item breakdown, these are the items that need to be replaced as part of the restoration of your property and includes the estimate from the insurance company for the scope of work for repair. This is a budgetary document so that the insurance company, contractor, and homeowner all know where the starting point is. Here, they break the different components of the claim into sections. You’ll see a drawing of a house, top-level numbers, then finally the line item breakdown.

The description details all the different services to preform, or materials that need to be replaced— different things that the adjuster says needs to occur on your project. The next column is quantity (SQ). SQ stands for 100 square feet which is simply how they measure roofing material, i.e. 30.62 SQ = 3,062 sq feet. When they tear off material there is usually more than the install because they are accounting for a particular factor for cut and waste. Next, there is the unit price for each square, and then the total (RCV). i.e. 36.62 SQ times the unit price of 56.25 results in the RCV (real cost value) of 1,712.38. Then there’s the deprecation amount, followed by the final column ACV (actual cost value), the value they’re including in the check.

The most important line for a homeowner is the bottom line: this is what your insurance company is paying to replace the roof.

Other Break-downs

Since we’re roofers, the examples we’ll discuss here will be about your roof, however, if occurred to other parts of your property, or other buildings on your property, each of those will be broken into their own sections. You may see sections such as the ones listed below:

Roof (or Dwelling Roof)

Detached Garage roof

Front, Right, Rear, Left Elevations

Gutters

Etc.

FILE #: 251833035

Sections of the House

The sections for the “elevations” are for the different sides of your house. They normally use Front, Right, Rear, and Left designations to avoid confusion related to directional designations like North, South, East, and West.

As the insurance adjuster goes around the house to find damage on those designated sections. It is a universal standard especially if there is a house that is a bit uneven. All of the work for each house side on the exterior will be shown underneath this particular breakdown.

That is, gutters, painting, window well cover etc. So, any work that is needed to be done on the exterior of every side it will be shown in the breakdown section for that side.

Do You Need To Understand All This Information?

Many of the terms and phrases used in the claim form pages will be foreign to the average homeowner. Don’t worry about it. If you’re working with a contractor, he will understand these line items, and in many cases, your contractor may also be using Xactimate.

What will matter the most for you to understand about these pages will be that all of these items make up the scope of loss that your adjuster thinks should occur to restore you to “like-kind-and-quality” of “pre-loss” condition.

This is also where your contractor may disagree with the adjuster. Whether your contractor uses Xactimate or not, he will likely have a line item break-down of all the components necessary to complete your repair. There may be items in your contractor’s estimate that aren’t in your insurance claim, or the items may be in the claim, but may be different, either in measurements or pricing. If so, this is where a supplement becomes necessary.

The claim form pages will also be a big benefit to you in another way. They will help you compare the different estimates you’re getting from roofers and will allow you to ask each one about the items that he has in his estimate that aren’t in your claim. A professional contractor will be able to give you the information and education about these missing items and explain why they’re necessary.

The main point to remember, though, is that just because your claim document doesn’t have items that your contractor has, doesn’t mean that you have to find a contractor who will only include items that are in your claim, or who will do your project for the price of the claim. As long as your contractor’s scope of work and costs are reasonable, within fair market value, and can be justified, your insurance company will adjust their claim.

FILE #: 13280377

Conclusion

The two most important pages for you as a homeowner is the first page that shows all of the actual dollar amounts and the actual estimate breakdown of your roof; net claim, replacement cost value, and deductible are really important numbers to know. The roof page is the most important piece for your roofing contractor.

I hope that this has helped to clear up some of the confusion you may have had about insurance claim form pages. If you have any more questions, please don’t hesitate to reach out to us and we’ll be happy to help!

We have more articles to come explaining additional information about your claim document and we’ll link to those here.

_____________________________________________________________________________________

Homestead Roofing has inspected, repaired, and replaced thousands of roofs in Colorado Springs and the surrounding counties.

As a family-owned business, we take every project personally, committing all our efforts to ensure you and your loved ones have an excellent roof for your living space. Contact us today for more information about our roofing solutions.